Free Insurance for Our Covered Call Trades: Making the Case for ITM Strikes – February 24, 2025

There are 2 major ways to protect the investment inherent in our covered call trades. On way is buy protective puts and convert the covered call trade to a collar trade. We must pay for this type of trade insurance. The other is to sell in-the-money (ITM) strikes, which have an additional intrinsic-value to the premiums. This form of insurance is paid for by the option buyer and free to us, the option seller. This article will analyze the benefits of ITM call strikes when taking defensive approaches to our covered call trades.

Option premium formula

Total premium = Intrinsic-value + time-value (extrinsic-value)

- Intrinsic-value (IV) applies only to ITM call strikes (lower than current market value)

- IV is the dollar amount the strike is lower than current market value

- At-the-money (ATM) and out-of-the-money (OTM) strikes consist of only time-value

- If a stock is trading at $48.00 and the $45.00 ITM call sells for $4.00, $3.00 is IV and $1.00 is time-value

- Because ITM strikes contain an IV component, the breakeven (BE) price points are lower than those for ATM and OTM call strikes

- This can be viewed as additional insurance for our covered call trades and is paid for by the option buyer, not us

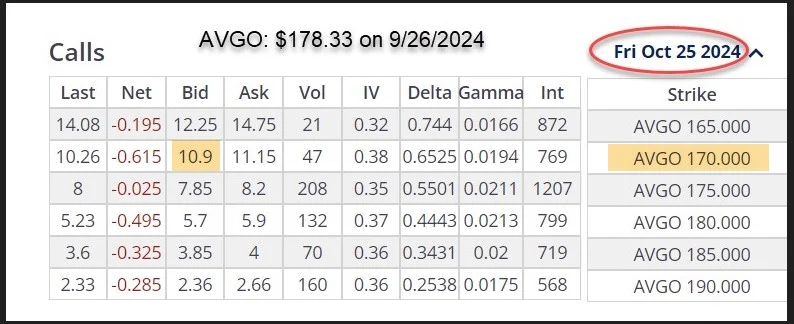

Real-life example with Broadcom Inc. (Nasdaq: AVGO): Option-chain on 9/26/2024

- 9/26/2024: AVGO trading at $178.33

- 9/26/2024: STO 1 x 10/25/2024 $170.00 ITM call at $10.90

- The BCI Trade Management Calculator (TMC) will break down the components of the trade premium

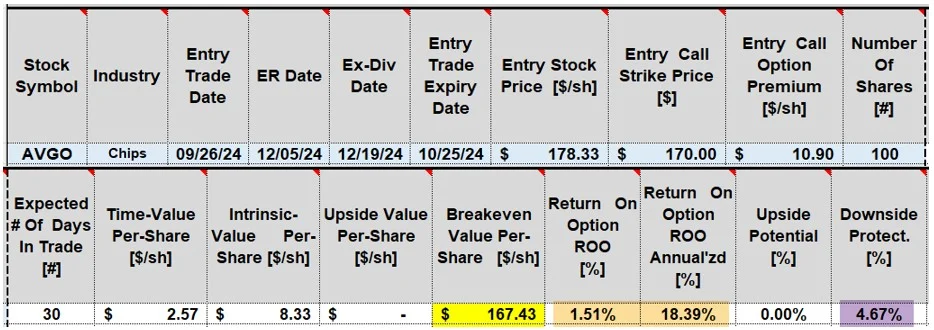

AVGO ITM covered call initial trade calculations with the BCI TMC

- The top section represents trade entries, and the lower section reflects spreadsheet calculations

- If the trade taken through contract expiration, this is a 30-day trade (lower left)

- The spreadsheet breaks down the premium into TV ($2.57) and IV ($8.33)

- The BE price point is $167.43 (yellow cell)

- The initial TV return is 1.51%, 18.39% annualized (brown cells)

- The downside protection is 4.67% (purple cell). This is our free insurance. It means that we are guaranteed a 1.51%, 30-day return, as long as share value does not decline by more than 4.67% at expiration. Intrinsic-value protects time-value, is another way to state this form of free insurance. This is different from the BE price point

Discussion

One of the many advantages of covered call writing is that we can leverage the concept of the money ness of the strikes to set up defensive trades where the additional insurance is paid for by the option- buyers, not us, the option-sellers.

Author: Alan Ellman