The Inverse Relationship Between Stock Price and Put Premium – March 3, 2025

When selling our cash-secured puts, understanding the correlation between stock price and our put premiums is critical to maximizing the success of our trades. For covered call writing, the relationship is direct … if share price increases, so will the value of our call options by its Delta factor. For puts, the opposite is true … if stock value rises, put value falls, providing us with the opportunity to buy back the put option at a much lower price. This is why when we view a put option chain, the stats have negative Deltas.

What is Delta?

One of the 3 definitions of Delta is the amount an option premium will change for every $1.00 change in the price of an underlying security. If we generate $1.00 per share when selling a cash-secured put and the strike has a Delta of -.50 per share or -50 for the contract, and share price changes by $1.00, then put value is reduced (if stock price rises) or increased (if stock price falls) by $0.50.

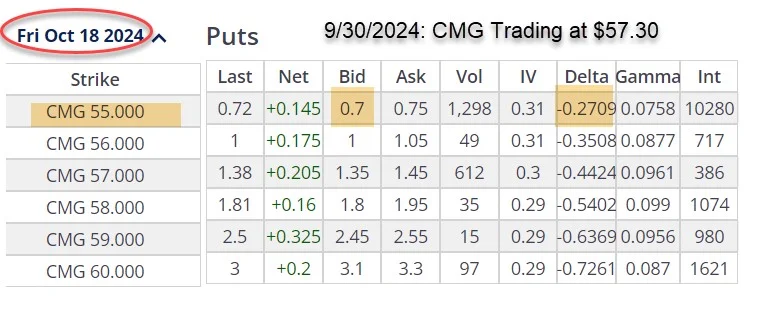

Real-life option-chain with Chipotle Mexican Grill, Inc. (NYSE: CMG)

- 9/30/2024: CMG trading at $57.30

- 9/30/2024: The 10/18/2024 $55.0 OTM put shows a bid price of $0.70

- 9/30/2024: The $55.00 put shows a Delta of -0.2709

- For every $1.00 in share price increase, the $0.70 premium will reduce in value by $0.27

- If the share price rises enough, we can buy back the option at an extremely reduced price and sell a higher put strike to generate additional option income (rolling-up)

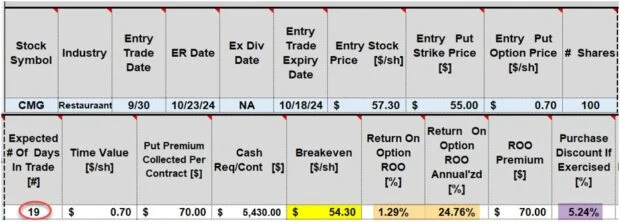

CMG initial put calculations using the BCI Trade Management Calculator (TMC)

- Red circle: If taken through expiration, this is a 19-day trade

- Yellow cell: The breakeven price point is $54.30

- Brown cells: The initial time value profit is 1.29%, 24.76% annualized

- Purple cell: If the put is exercised and shares are put to us, we buy those shares at a 5.24% discount from the price at trade entry (the breakeven price of $54.30-yellow cell)

What are the 20%/10% guidelines for cash-secured puts?

These are exit strategy guidelines which assist us in determining when to buy back our cash-secured puts when the share price accelerates significantly. In the first half of a monthly contract, we enter a buy-to-close (BTC), good-until-cancelled (GTC) limit order of $0.14 (20% of $0.70) after selling the CMG cash-secured put. In the last 2 weeks of a monthly contract, we change the limit order to $0.07, 10% of $0.70. This is also a BTC/GTC limit order. If we can retain 80% – 90% of our original option premium and generate more than $014 or $0.07 by rolling up to a higher put strike, we will have generated an additional income stream or perhaps more.

Discussion

When selling cash-secured puts, we can generate additional income streams by understanding the inverse relationship between share price and put value. Using the BCI 20%/10% guidelines will partially automate the exit strategy process.

Author: Alan Ellman