The Poor Man’s Covered Call: Can We Use ITM Covered Call Strikes? – March 17, 2025

What is the Poor Man’s Covered Call (PMCC)?

This is a covered call writing-like strategy where LEAPS options are purchased instead of the actual stocks or ETFs and short calls are written against these long positions. LEAPS options expire approximately 9 – 24 months out. The technical term is a long call diagonal spread. It is generally considered a long-term strategy where weekly or monthly income is generated by selling OTM covered calls against the long option positions. I have seen this strategy defined as “covered call writing, but cheaper”. Please do not accept this interpretation as there are so many moving parts to the strategy that sets it apart from traditional covered call writing, both positive and negative.

Strike selection for our short calls

Typically, OTM weekly or monthly calls are used to both generate cash flow and to allow for share appreciation up to the OTM strike. BCI developed the PMCC Calculator which provides initial trades calculations and allows for trade management. When the considered trade is entered into the spreadsheet, a bold red “YES” or “NO” will appear, letting us know if this is an acceptable PMCC trade. Many of our members have noticed that OTM strikes generate “YES” more frequently than ITM strikes, which almost never calculate a “YES”.

What is the BCI trade initialization formula?

This is an algorithm inherent in the BCI PMCC calculator which answers the question: If we are forced to close the trade due to significant share appreciation, will we close at a profit? The formula is: [(Difference between the 2 strikes) + short call premium] > Cost of LEAPS

This formula is particularly useful to protect against auto-exercise when short call strikes are ITM near expiration.

Based on this formula, OTM strikes will provide a much greater credit on the left side of the equation than ITM strikes, because the difference between the strikes is much larger.

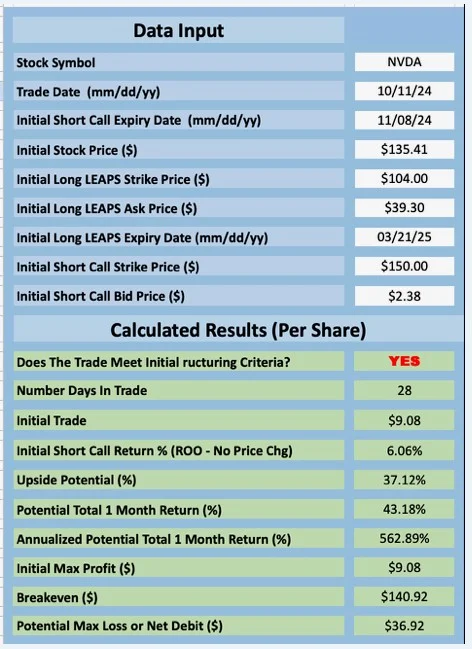

Real-life OTM example with NVIDIA (Nasdaq: NVDA)

- With NVDA trading at $135.41 on 10/11/2024, the 3/21/2025 $104.00 LEAPS cost $39.30

- The OTM 11/8/2024 $150.00 call generated a premium of $2.38

- If closed, the net credit would be $9.08 per-share, resulting in a bold red “YES” in the spreadsheet

- This initial PMCC trade resulted in an initial time-value return of 6.06% with an additional 37.12% of upside potential

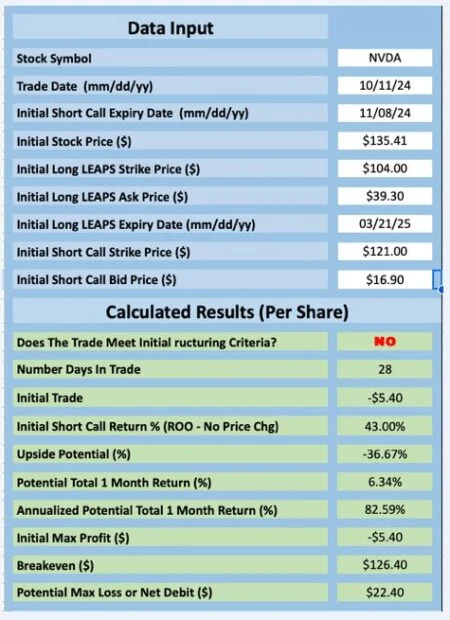

Real-life ITM example with NVIDIA (Nasdaq: NVDA)

- With NVDA trading at $135.41 on 10/11/2024, the 3/21/2025 $104.00 LEAPS cost $39.30

- The ITM 11/8/2024 $104.00 call generated a premium of $16.90

- If closed, the net debit would be $5.40 per-share, resulting in a bold red “NO” in the spreadsheet

- This initial PMCC trade resulted in an initial time-value return of 6.06% (if share price moved below the $121.00 strike, resulting in no exercise) with no upside potential

Discussion

The PMCC strategy, generally, incorporates deep ITM long LEAPS options and slightly OTM short (covered) call options. Using this combination allows us to align with the BCI PMCC trade initialization formula which assures of a winning trade if share price accelerates substantially early in the trade.

Author: Alan Ellman